What if everything goes right?

While equities have headroom in a benign environment, we now see credit as unfavourably asymmetrical given limited risk compensation and capped upside.

The below is an extract from our Q3 Asset Allocation outlook.

In January we shifted our base-case thesis from a mid-year recession to an uneasy status quo vulnerable to any deviation from the soft-landing narrative.

This evolution of our thinking has continued throughout the year, reflecting what we’re seeing in markets and our beliefs about the best ways of finding value in the various possible scenarios.

The macro backdrop: staying on that narrow path

Consensus growth forecasts for the US were revised higher earlier in the year, mainly reflecting an abandoning of recession calls by the pessimists rather than an upgrade from the optimists. This left consensus strongly clustered around a US soft landing.

In recent weeks the upside surprises have given way to more mixed reports. This has helped reduce concerns around a possible ‘no landing’ and inflation, but has not been sufficiently weak to create renewed worries about a hard landing. The Federal Reserve has signalled only one cut this year in its June dot plot, but it’s worth remembering that there are still three more inflation readings to come before the September meeting.

Across Europe, consensus forecasts have been relatively stable over the past few months as the gradual recovery from stagnation last year has proceeded largely as expected.

The data have been supportive of a benign rebalancing, but we still see limited slack across developed markets and overconfidence among economists and markets that the path forward will remain smooth. Geopolitics could still surprise, especially when combined with fragile fiscal positions in many countries, as we have seen recently in France.

In terms of central banks, the mean outcomes embodied in market pricing seem appropriate at present. If growth does not slow in the US or picks up further in Europe, inflation risks are skewed to the upside. But if unemployment rises, central banks would likely be quick to cut. So, a once-a-quarter path for rate cuts seems reasonable, even if we have low conviction around this being the ultimate path. We also think it will be difficult for central banks to meaningfully diverge from one another.

How we’re positioned: short credit

We believe markets remain vulnerable, but this idea has not worked so far, and it’s hard to see a catalyst for a shock to the narrative (famous last words). Consider the evidence:

- Sentiment and positioning indicators remain far from extreme, which is at odds with our ‘vulnerable market’ thesis

- Aggregate earnings projections, once we adjust for tech megacaps, don’t look unduly challenging. Nvidia* earnings, a bellwether for the AI theme, once again came in better than expected

- Wage growth keeps moderating despite our earlier assertions that this was unlikely without a rise in unemployment

- We believe profit margins will be squeezed as nominal growth slows, but we’ve been waiting a long time given that nominal growth has been slowing since late 2021

- Inflation stickiness has been apparent in recent months, but the bigger picture is that inflation has fallen back to fairly comfortable levels without much economic pain

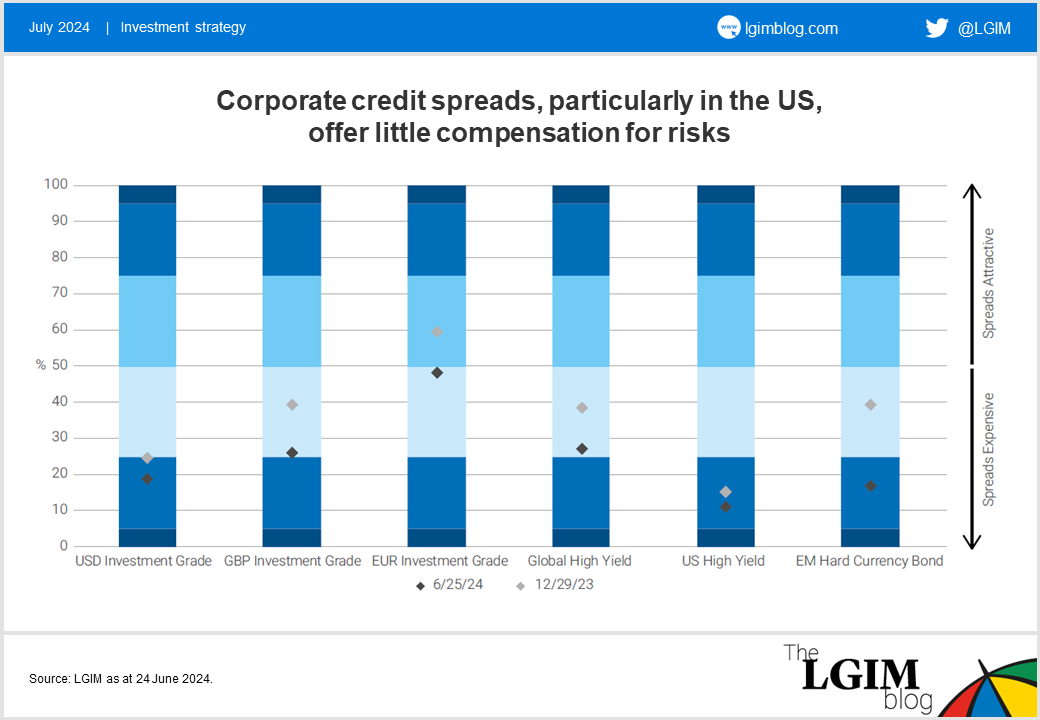

So, we’ve adapted our short risk position, closing the equity short while increasing the credit short. We want to remain short risk but predominantly in credits now as credits have less upside risk than equities.

We’ve been waiting for spreads to stabilise around current levels before going further underweight. We know that selling too early can be costly in terms of carry accrual. But we think we are getting very close to that point as the pace of credit outperformance has slowed dramatically. Looking just at USD investment grade, spreads tightened 20 basis points (bps) in Q423, 10bps in Q1 this year and just 3bps in the first couple of months of Q2.1

We also worry that credit excess returns will start to lag behind equities on a risk-adjusted basis from here, consistent with the historical precedent. The potential for speculative excess in an asset class offering capped upside is limited.

This quarter’s articles: from the mainstream to the unfamiliar

This quarter’s outlook features a wide range of our thinking, from widely discussed topics that just won’t go away to more esoteric parts of the investment world that we feel deserve attention.

In the former camp is Andrzej and Robert’s piece on the seemingly unstoppable rise of US tech stocks, and how to guard against a momentum reversal. Camilla and Patrick, meanwhile, question whether London has lost its appeal as a listing location, and what it would take for valuations to rebound.

Willem heads into less familiar territory in his article, examining the role of alternative risk premia (ARP) strategies and what we’ve learnt about them in the near-decade we’ve been integrating them into some of our multi-asset portfolios.

Tim rounds out this quarter’s update with his regular CAMERA feature showing our long-term return expectations across a range of assets, this time with a focus on the UK.

The above is an extract from our Q3 Asset Allocation outlook.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an

LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

1. Source: Bloomberg data as at 20 June 2024.

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally invested. Past performance is no guarantee of future results.

Whilst LGIM has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

The risks associated with each fund or investment strategy should be read and understood before making any investment decisions. Further information on the risks of investing in this fund is available in the prospectus at. http://www.lgim.com/fundcentre

Key risks

The value of any investment and any income taken from it is not guaranteed and can go down as well as up, and investors may get back less than the amount originally invested.

Whilst we have incorporated ESG information into investment decision making and stewardship practices, there can be no assurance that any responsible investing goals will be met.

Author(s)

Emiel van den Heiligenberg

Head of Asset Allocation